Tickets can have a big impact on your car insurance. When you get a ticket, insurance companies take notice. They use this information to decide how much you’ll pay for coverage.

Have you ever wondered if your insurance company knows about that speeding ticket you got last year? Or maybe you’re curious about how your driving record affects your insurance costs. These are common questions many drivers have.

In this article, we’ll explore how insurance companies check your driving record. We’ll also look at how tickets and other driving issues can change your insurance rates. By the end, you’ll have a better understanding of how your driving choices impact your insurance.

How Insurance Companies Get Your Driving Information?

Insurance companies need to know about your driving habits. They use this information to decide how much to charge you for insurance. But how do they get this information? Let’s look at some ways they find out about your driving history.

One way insurance companies learn about your driving is through your state’s Department of Motor Vehicles (DMV). Most insurance companies have agreements with DMVs. These agreements let them access driving records. When you apply for insurance, the company can check your record with the DMV.

Another way insurance companies get information is from you. When you apply for insurance, you’ll be asked questions about your driving history. You might need to tell them about recent tickets or accidents. It’s important to be honest because the insurance company will likely check your answers against official records.

Insurance companies also use special reports to learn about your driving. These reports, like the C.L.U.E. report, show information about your insurance claims. They can see if you’ve had accidents or other issues that led to insurance claims. This helps them understand how risky you might be as a driver.

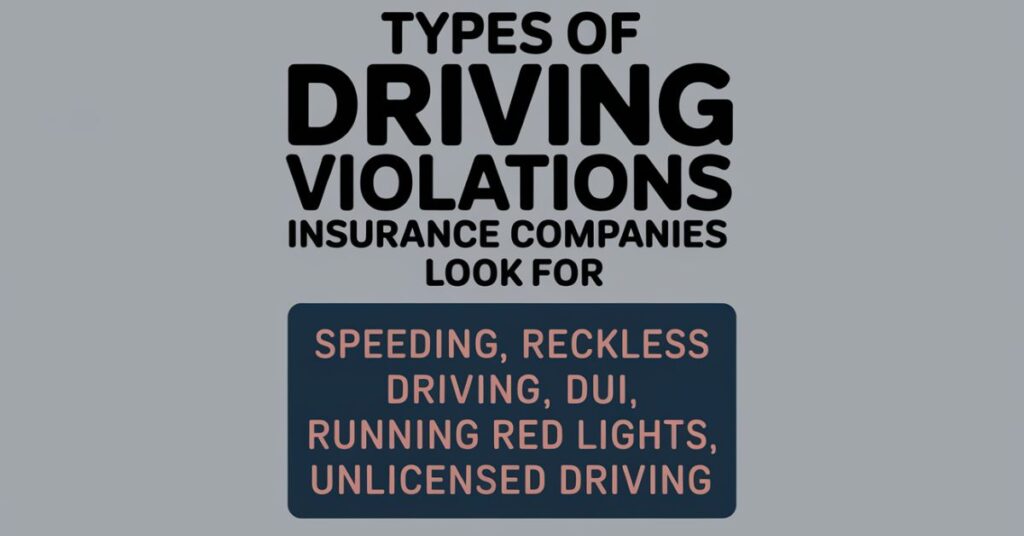

Types of Driving Violations Insurance Companies Look For

Insurance companies care about different types of driving violations. Some violations are seen as more serious than others. The type and number of violations on your record can affect your insurance rates. Let’s look at what kinds of issues insurance companies pay attention to.

Speeding tickets are one of the most common violations insurance companies see. If you have one or two minor speeding tickets, it might not affect your rates much. But if you have many speeding tickets or were caught going way over the speed limit, your rates could go up a lot. Insurance companies see speeding as risky behavior that could lead to accidents.

Drunk driving or driving under the influence (DUI) is taken very seriously by insurance companies. If you have a DUI on your record, your insurance rates will likely go up a lot. Some companies might even refuse to insure you. DUIs show that a driver makes dangerous choices, which makes them very risky to insure.

Other violations insurance companies look at include running red lights, not wearing a seatbelt, and distracted driving (like using your phone while driving). These show that a driver might not be following safety rules. Even if these don’t cause immediate accidents, they make insurance companies worry about your driving habits.

How Far Back Do Insurance Companies Look?

Insurance companies don’t look at your entire driving history forever. They usually focus on recent years. Here’s what you need to know about how far back they check:

- Most insurance companies look at the last 3 to 5 years of your driving record.

- Serious violations like DUIs might be considered for longer, sometimes up to 10 years.

- Some states have laws about how long violations can affect your insurance rates.

- Very old tickets or accidents usually don’t affect your current insurance rates.

- New drivers with short histories might have their entire record considered.

Factors That Affect Your Insurance Rates

When insurance companies set your rates, they look at many things. Your driving record is just one part of the picture. Let’s explore some other factors that can change how much you pay for insurance.

1. Your Age and Driving Experience

Young drivers often pay more for insurance. This is because they have less experience on the road. Insurance companies see them as more likely to have accidents. As you get older and have more years of driving, your rates might go down. This is if you keep a clean driving record.

2. The Type of Car You Drive

The car you drive matters to insurance companies. Some cars are more expensive to repair or replace. Others are more likely to be stolen. If you drive a car that’s seen as safer, you might pay less for insurance. Sports cars or luxury vehicles often cost more to insure.

3. Where Do You Live?

Where you live can affect your insurance rates. If you live in a city with lots of traffic, you might pay more. This is because there’s a higher chance of accidents or theft. Rural areas might have lower rates because there are fewer risks.

4. Your Credit Score

In many states, insurance companies can look at your credit score. They believe that people with higher credit scores are less likely to file claims. If you have a good credit score, you might get lower insurance rates. This is true even if your driving record isn’t perfect.

5. How Much You Drive?

The more you drive, the more chances you have of getting into an accident. If you don’t drive very much, you might pay less for insurance. Some companies offer low-mileage discounts. This is good for people who don’t use their cars a lot.

How Tickets Affect Your Insurance Rates?

Getting a ticket can change how much you pay for insurance. But not all tickets are the same. Let’s look at how different tickets might affect your rates.

Minor speeding tickets might not change your rates much. If it’s your first ticket and you weren’t going too fast, some companies might not raise your rates at all. But if you get many tickets or were speeding a lot, your rates could go up.

More serious violations like reckless driving can cause big increases in your rates. These show insurance companies that you’re taking big risks on the road. They might think you’re more likely to cause an accident, so they charge you more.

The most serious violations, like DUIs, can double or triple your insurance rates. Some companies might even cancel your policy. If this happens, you might need to look for high-risk insurance, which is much more expensive.

Read this article: Does DUI Insurance Have to be Claimed Before Conviction?

Ways to Improve Your Driving Record

If you have tickets or accidents on your record, don’t worry. There are ways to improve your situation. A table showing some steps you can take:

| Action | How It Helps | Time to See Results |

| Take a defensive driving course | Can remove points from your license | Immediate to a few months |

| Drive safely for a long time | Shows you’re a responsible driver | 3-5 years |

| Contest tickets in court | Might get tickets removed from your record | Varies |

| Ask about accident forgiveness | Some companies won’t count your first accident | Immediate if offered |

| Improve your credit score | Can lower rates in many states | 6 months to a year |

How Often Insurance Companies Check Your Record?

Insurance companies don’t check your driving record every day. But they do look at it more often than you might think. Let’s explore when and why they might check your record.

Most insurance companies check your record when you first apply for insurance. This helps them decide if they want to insure you and how much to charge. They look at your recent history to see if you’re a risky driver or a safe one.

Many insurance companies also check your record when it’s time to renew your policy. This usually happens once a year. They want to see if anything has changed. If you’ve gotten tickets or had accidents, your rates might go up at renewal time.

Some insurance companies do random checks throughout the year. They might do this to see if you’ve had any new violations. If they find something, they could raise your rates before your renewal. But this isn’t very common. Most companies wait until renewal time to make changes.

What to Do If You Get a Ticket?

Getting a ticket can be stressful. You might worry about how it will affect your insurance. Some steps you can take if you get a ticket.

1. Don’t Panic

First, don’t panic. One ticket doesn’t always mean your insurance will go up. Many companies have forgiveness programs for first-time offenses. Take a deep breath and look at your options before assuming the worst.

2. Decide Whether to Fight the Ticket

You can choose to fight the ticket in court. If you win, the ticket won’t go on your record. This means your insurance company won’t see it. But fighting a ticket takes time and might cost money. Think about whether it’s worth it based on the type of ticket.

3. Take a Defensive Driving Course

Some states let you take a defensive driving course to remove points from your license. This can help keep your insurance rates from going up. Check with your local DMV to see if this is an option for you.

4. Be Honest with Your Insurance Company

If you do get a ticket, be honest if your insurance company asks about it. Lying can lead to bigger problems. Your company might find out anyway, and being dishonest could cause them to cancel your policy.

5. Shop Around for New Insurance

If your rates do go up because of a ticket, you can shop around. Different companies treat tickets differently. You might find a better rate with a new company, even with the ticket on your record.

The Role of Insurance Agents

Insurance agents can be helpful when dealing with tickets and insurance rates. Let’s look at how they can assist you.

An insurance agent can explain how tickets might affect your rates. They know the rules for their company and can give you a good idea of what to expect. This can help you plan for any changes in your insurance costs.

Agents can also tell you about programs that might help. For example, they might know about safe driver discounts or accident forgiveness programs. These can help keep your rates low even if you have a ticket.

If you’re worried about your driving record, talk to your agent. They might be able to suggest ways to improve your situation. This could include taking driving courses or waiting for tickets to fall off your record.

Tips for Keeping Your Insurance Rates Low

Even if you have tickets, there are ways to keep your insurance rates as low as possible. Some tips to help:

- Drive safely and avoid getting more tickets.

- Take advantage of all discounts offered by your insurance company.

- Consider raising your deductible if you can afford it.

- Bundle your car insurance with other types of insurance.

- Improve your credit score if your state allows it to be used for insurance rates.

Final Words

Insurance companies do check to see how many tickets you have. They use this information to decide how much to charge you for insurance. Tickets can make your insurance cost more.

But there are things you can do if you have tickets on your record. You can take defensive driving courses and be extra careful on the road. Over time, old tickets will fall off your record.

Remember, the best way to keep your insurance costs low is to drive safely. Avoid getting tickets in the first place. This will help you keep a clean driving record and lower insurance rates.

Frequently Asked Questions

How long does a ticket stay on my insurance record?

Most tickets stay on your insurance record for 3 to 5 years. Serious violations like DUIs might affect your rates for longer.

Will my insurance rates go up for one speeding ticket?

It depends on the company and how fast you were going. Some companies forgive the first minor ticket.

Can I hide tickets from my insurance company?

No, it’s not a good idea to try to hide tickets. Insurance companies can check your driving record and lying could lead to cancelled insurance.

How often do insurance companies check driving records?

Most companies check when you apply for insurance and at each yearly renewal. Some might do random checks.

Can I get lower rates after having tickets on my record?

Yes, as time passes and you drive safely, your rates can go down. You can also look for companies that offer better rates for your situation.

David: Seasoned financial expert with 5 years in banking and investments.

Skilled in personal finance, market analysis, and wealth management. Empowers clients to achieve financial goals.